Hi Friends,

I hope you all had a great Lunar New Year. As we move into the second month of the year we have started to see more buyers pop up in the LA market. This is because rates have surprisingly started to slowly go down. More and more properties are going through price reductions which is another main factor buyers are starting to emerge.

If you are thinking of buying or selling a property, I would love to help. I am always here to answer any questions you may have.

Check out Barronestates.com for more information on selling, purchasing or leasing your next home.

I will do my best to assist and educate you in finding your place called “Home, Sweet Home” for now or at last!!

Warmest Regards,

Oriana

I am humbled and excited to announce I was awarded the Coldwell Banker Realty International Sterling Society Award for outstanding production in 2022. Thank You to all my clients, colleagues, management, family and friends for all your endless love & support. This truly means the world to me.

![]()

The average rate for a 30-year mortgage dropped to 6.15% last week — the lowest in 18 weeks.

This dip in rates provides welcomed relief for many potential homebuyers who’ve put their dreams on pause thanks to high mortgage interest rates, which have drastically reduced their buying power.

On top of reduced interest rates, the Federal Housing Finance Agency (FHFA) has announced changes to its fee structure beginning May 1, 2023. These changes affect conventional loans and will reduce the cost of a loan for certain borrowers (while increasing it for others).

Plus, according to Redfin, average home prices in the U.S. have continuously dropped, albeit slowly, since hitting their peak in May 2022.

With rates lower than they have been and fee changes coming down the pipeline, it’s a good time to reassess the home-buying plans you may have put on hold and decide if now is the time to act.

Is now a good time to lock-in your mortgage rate?

If a painfully-high interest rate was the only thing holding you back from signing a mortgage, then you may want to jump on today’s (relatively) low rates. The Federal Reserve has been steadily increasing its benchmark Federal Funds rate and has signaled its intent to continue this pattern until inflation is under control. As long as the Federal Funds rate stays high, so will mortgage rates.

The recent dip in rates represents a significant savings for home buyers. Today’s 30-year mortgage rates are currently 0.93% lower than they were last fall, when rates hit 7.08%. For a $500,000 home loan, a 0.93% lower rate saves you $300+ on your monthly payment and over $110,000 in interest over the life of the loan.

To get the lowest interest rate on your mortgage, however, you’ll want to make sure your credit score is as high as possible. This may be the most-important step you can take when trying to get the best terms on a mortgage.

But before committing to buying a home, you’ll need to save up money for a down payment and closing costs. These upfront costs can easily add up to 10%- 20% of the home’s purchase price. On top of that, it’s a good idea to have money set aside for maintenance, repairs and moving costs. You’ll need to make sure you have enough money saved up before starting your home search.

One way you can reduce some of the upfront costs of buying a home is to compare offers from lenders that don’t charge origination fees. Here are some of the best lenders with no origination fees according to our rankings:

How will the upcoming fee changes impact me?

The upcoming FHFA fee changes affect conforming conventional loans, which can be sold to Fannie Mae or Freddie Mac by lenders. More niche mortgages, such as jumbo loans, FHA loans and VA loans will not be affected by these changes.

The specific fees that are changing are known as Loan Level Price Adjustments (LLPAs), which are risk-based fees applied to loans. Lenders base these fees on factors such as the borrower’s credit score, the loan-to-value ratio (LTV) and the type of mortgage. In general, you’ll pay more if your credit score is lower or if you’re borrowing a higher percentage of the property’s value (i.e. higher LTV).

The future fee changes will add an additional layer of complexity to a process that already causes heads to spin. For example, the LLPAs for a purchase mortgage will drop for some borrowers with lower credit scores, while borrowers with higher credit scores could be paying more in certain circumstances.

Given the amount of nuance with LLPAs, it’s important to have a conversation with your lender (or multiple lenders) to see how the upcoming changes could affect your home loan. Keep in mind that although the changes apply to loans sold to Fannie Mae or Freddie Mac from May 1, 2023, lenders will begin adjusting their fees well before that deadline.

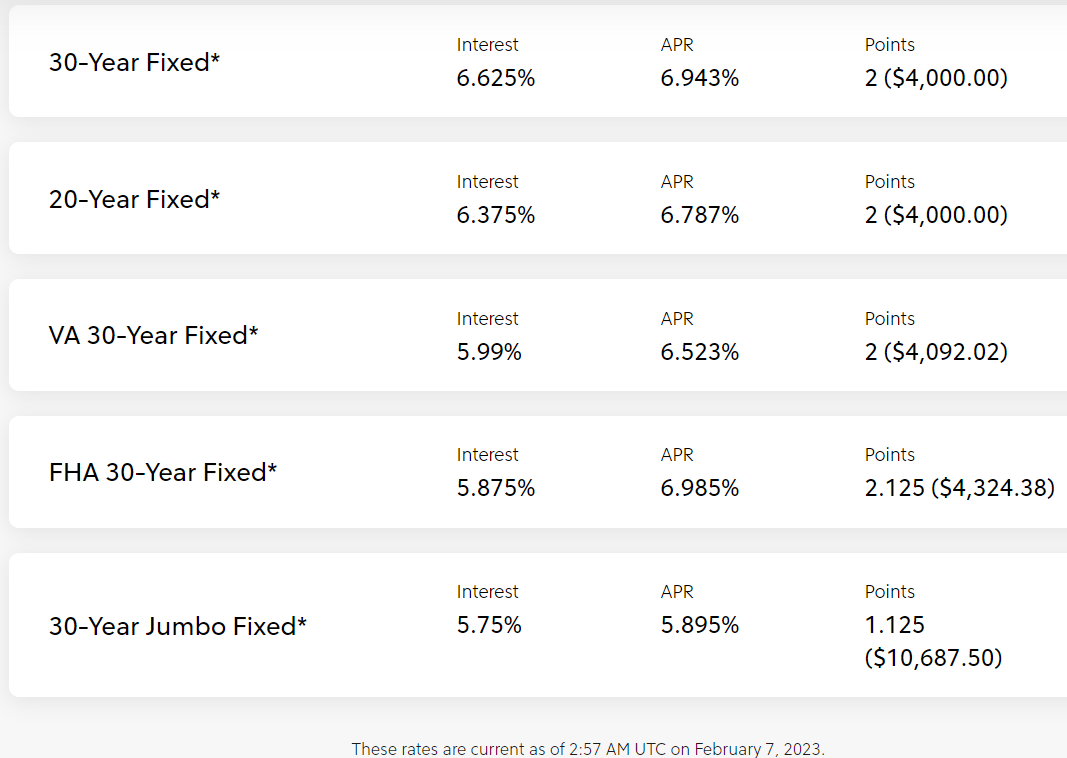

You can see the current fees here and the upcoming fee structures here.

Bottom line

Mortgage rates have dipped in recent weeks, which can help make your future mortgage payments more affordable. Just be sure to pay attention to the fees, in addition to the rate, when you are comparing mortgage loan offers.

Also, certain fees associated with conventional loans are changing soon, which could save you money or cost you more depending on your situation. So if you’re in the process of buying a home, talk with your lender to figure out how you’ll be affected.

![]()

Homes are selling at their slowest pace since the housing market nearly ground to a halt at the beginning of the pandemic, according to a new report from Redfin, a technology-powered real estate brokerage.

The typical home that sold during the four weeks ending January 8 was on the market for 44 days, the longest time span since April 2020, contributing to the biggest annual inventory increase on record. Pending home sales dropped 32% year over year to their lowest level on record and mortgage-purchase applications dropped to their lowest level since 2014.

High mortgage rates and extreme winter weather at the start of the year deterred would-be home buyers, exacerbating the typical holiday slowdown. But there are signs that early-stage demand is up. Redfin’s Homebuyer Demand Index–a measure of tour requests and other buying services from Redfin agents–posted a 6% increase over the last month, and Google searches for “homes for sale” are on the rise. Some buyers are likely coming in from the sidelines because mortgage rates have dropped to 6.33% from their November peak of over 7%, saving the typical buyer roughly $250 on monthly housing payments.

Buyers may also be encouraged by signs of improvement in the economy, with inflation easing in December for the sixth month in a row as wage growth softens. “We’re entering 2023 with positive economic news,” said Redfin deputy chief economist Taylor Marr. “The latest consumer price index report confirms that the worst of inflation is behind us. That means the Fed is likely to continue easing its interest rate increases, which should cause mortgage rates to continue gradually declining. This could bring back some home buyers in the coming months. We’ve already seen an uptick in people initiating home searches. Although those house hunters haven’t yet turned into buyers, they may soon given that monthly mortgage payments are notably down from their peak and the latest inflation and employment data lower the chances of a recession.”

Home prices fell from a year earlier in 20 of the 50 most populous metros

The typical home sold for $351,250 during the four weeks ending January 8. That’s up 0.8% from a year earlier, but down about 10% from the June peak. Prices fell year over year in 20 of the 50 most populous metros. By comparison, 11 metros saw price declines a month earlier.

Prices fell 10.6% year over year in San Francisco; 5% in Seattle; 4.9% in San Jose; 4% in Austin; 3.8% in Detroit; 3.7% in Phoenix; 3.4% in Oakland, California; 3% in Boston; 3% in Los Angeles; 3% in Sacramento; 2.6% in San Diego; and 2.5% in Chicago. They fell 2% or less in Portland, Oregon; Anaheim, California; Riverside, California; Newark, New Jersey; New York; Pittsburgh; Las Vegas; and Washington, D.C.

This marks the first time Las Vegas prices have dropped year over year since at least 2015. It’s the biggest year-over-year price drop in San Francisco, Seattle, Phoenix, Chicago, Boston, Portland and San Diego since at least 2015.

Lady and the Tramp had the right idea—what better way to celebrate with your significant other than sharing a romantic meal? Whether you’re looking to wine and dine on a rooftop, cozy up on a first date or splurge to celebrate a special occasion, we’ve got you covered with a round-up of L.A.’s best restaurants that lay on the charm. Below, check out our guide to the best romantic restaurants in Los Angeles.

Hoping to impress your honey on V-Day? Our guide to Valentine’s Day ideas for couples has a bevy of romantic things to do to help you get closer. With romantic meals and spa days back on the table this year, it’s a little overwhelming right now to sort out a standard date night plan from a Valentine’s-worthy one. But not to worry: These are the best (and, in most cases, relatively budget-friendly) ways to turn L.A. into a romantic city this Valentine’s Day.

“New Look” Barronestates.com

If you’re new to the newsletter or haven’t joined us in a while, I have a brand new website that is an amazing tool if you’re looking to purchase a home. I worked this past year at bringing a new and improved site to all of my clients and future clients. The site is much easier to navigate and allows users to search for properties directly through my site. You will also be able to access all previous newsletters as well as the current one. My goal is to provide a better user experience for everyone to make finding or selling their dream home a success. Please visit Barronestates.com for a new and improved user experience! THANK YOU for all your continued support!

READY TO LIST OR FIND YOUR NEXT HOME?

Contact Oriana & learn more at BarronEstates.com